Submitted by Thomas Kolbe

Save in times of plenty, and you’ll have in times of need. An old German proverb, now proving tragically prophetic. The hardship caused by a completely derailed climate-socialist ideology is only just beginning. This socialist experiment is likely to continue ravaging the country until its economic substance is entirely consumed.

The new year begins as the old one ended: a fiscal raid on the wallets of the middle class. In Brussels and Berlin, there is satisfaction that citizens have been quietly, without spectacle, subjected to yet more tax increases—whose revenues, like a rising tide, lift all ships only slightly.

On January 1, the CO₂ price per ton of emitted gas rose from €55 to €65. This levy, applied to fossil fuels such as gasoline, diesel, natural gas, and heating oil, threads like a red line through the entire value chain—even reaching private households’ bills. The green extraction mechanism is now firmly entrenched, funding Brussels’ expanding activities increasingly, and is defended tooth and nail by the ruling politicians.

The Lie of Tax Relief

When the federal government celebrates its minimal tax relief for lower- and middle-income groups, reality tells a different story. In truth, these relentless fiscal collectors are increasing the tax burden further. Only the distracting work of state-affiliated media prevents the growing hyperstate’s costs from becoming fully visible.

2026 is set to become an expensive year for Germany’s shrinking middle class, visible soon on the first paycheck of the year. That will reveal the true cost of an overextended welfare state and the one-of-a-kind experiment of transforming Germany’s social insurance system into a quasi-global insurance scheme.

Never since World War II has the German middle class faced such fiscal and economic pressure.

The Burden of State Subsidies on the Middle Class

The countless subsidies and state interventions financing the complex “green arts” sector, the Ukraine war, and now the military buildup constitute a direct attack on the German middle class. Businesses and net taxpayers pay an ever-rising “blood price” each year to sustain Berlin’s and Brussels’ ideological and power ambitions.

The still-active renewable energy subsidy program, the EEG, alone consumes over €16 billion this year for an energy grid that, since the end of nuclear power, no longer provides a secure base for industrial production, sending both industrial and household electricity costs to dizzying heights. Trittin’s “ice ball” has become a cost Himalaya no one can climb.

Germany’s seven-year industrial decline, which is now accelerating, precisely chronicles the path of the deliberate destruction of its industrial base. Nearly 300,000 industrial jobs have been lost since 2018—tragic, yet apparently of little concern to Berlin’s policymakers.

Local city treasurers, however, are feeling the pain: as corporate tax revenues collapse under industrial destruction, citizens can expect cuts in public services and steep tax hikes. Schools, kindergartens, sports facilities—all face drastic savings. A big “thank you” goes to Berlin central planning.

Industry on the Edge: Loans Fizzle

What Friedrich Merz, Ursula von der Leyen, and other central planners aim for is clear: using state loans to occupy freed-up industrial capacities. Yet no matter how much funding flows into the new social program under the banner of a special fund for green and military production—the effect has already fizzled. In December, the entire Eurozone industrial sector, measured by current Purchasing Managers’ Indices (PMI), slipped into recession. Germany has been continuously downsizing its industry for seven years.

A victory for Brussels’ central planners, whose goal appears to be the economic and geopolitical neutralization of the country. After years of deindustrialization and waves of bankruptcies, this strategy is hard to interpret otherwise. Germany’s PMI now sits at 47 points—clearly in contraction. Hundreds of thousands of jobs will be lost this year. Last year alone, 24,000 companies went bankrupt. Exact figures for job and net direct investment outflows are not yet available; in 2024, €64.5 billion flowed out of Germany. German industry is no longer competitive.

Quick Blame Game

The culprits are quickly identified. U.S. tariffs, a favorite topic of sympathetic media, are often cited, though the crisis began long before Donald Trump. Dumping competition from China is also highlighted. While this is a factor, 99 percent of Germany’s economic problems are homegrown.

No one forced the country to keep its borders wide open for a decade, pushing its social insurance to the brink of collapse—all to create new voter bases for the united political left and to break resistance from the bourgeois right.

Shrinking Middle Class and Falling Investments

This trend is reflected in the middle class. The DATEV SME Index shows falling real revenues across all sectors, particularly trade, construction, and consumer services. Investments are nearly frozen: only 20 percent of companies plan rising investments, according to LBBW’s SME radar for the coming year.

The ideological green agenda has left its mark. High electricity costs, falling incomes, and persistent inflation are bleeding the middle class dry. Retail felt this for the first time during Christmas: nominal sales rose 1.5 percent, yet real sales fell by 1 percent in the peak month.

Economic stress will be a constant companion for Germany’s middle class in 2026. High property prices, zero real interest on savings, and rapid erosion of economic substance collide with an ever-expanding state. Bureaucracy and the state apparatus are evolving into a parasitic leviathan, funded by a shrinking number of contributors.

Consequences for Industry, Trade, and City Centers

Too much depends on Germany’s high industrial value creation: service businesses, high factor incomes, and secure municipal finances—all are now being lost, reflected in city centers.

Where once life flourished, roughly 5,000 retailers die every year, an irretrievable loss. The desolation mirrors what citizens feel in their wallets: the ebb has begun.

The middle class’s evaporating purchasing power is most visible in hospitality, where families cut costs first. Hotels lost 3.7 percent in real revenue in 2025, while restaurants and bars fell 4.1 percent year-on-year. Households are saving wherever possible. High energy costs, rising social charges, and a weakening job market leave a trail of economic decline.

Missed Lessons: The Population and the Crisis

Structural economic crises take time to penetrate public consciousness. Most households first tighten belts without complaint.

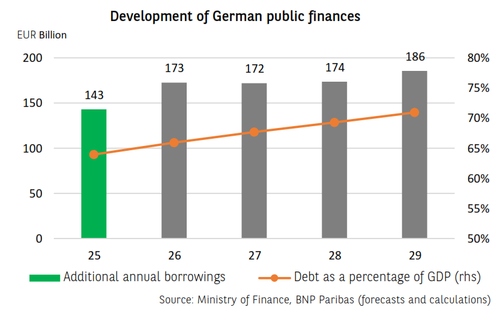

The state exploits this calm before the storm to consume citizens’ wealth faster than the private sector can compensate. With net new debt over 5.5 percent this year—including accounting tricks—this is particularly evident. The devotion of a portion of the population to ideological doctrine becomes an expensive, destructive tragedy.

Germany faces a nation unprepared to draw necessary lessons: reversing migration policy, adapting the bloated state apparatus to new economic realities, and downsizing accordingly. A turn toward a meritocratic market economy remains absent.

Until these lessons are learned and acted upon, Germany will continue to fall.

* * *

About the author: Thomas Kolbe, born in 1978 in Neuss/ Germany, is a graduate economist. For over 25 years, he has worked as a journalist and media producer for clients from various industries and business associations. As a publicist, he focuses on economic processes and observes geopolitical events from the perspective of the capital markets. His publications follow a philosophy that focuses on the individual and their right to self-determination.

{kind=link}

{kind=link}

{kind=link}

{kind=link}